A lot of people think (even me, once upon a time) that buying a second home to rent on Airbnb is a savvy business move, and in theory, it makes sense.

Thanks to the explosion in popularity of Airbnb, it seems like buying that second home is an easy way to earn extra income without going through the rigmarole of the traditional rental listing and leasing process.

Moreover, Airbnb historically comes with way fewer rules, regulations, and costs when compared to traditional rentals—this was especially true when the platform launched way back around the Great Recession (2008ish).

But today’s Airbnb is a whole lot different than the Airbnb of years ago. In fact, it’s pretty darn different from the Airbnb of even five years ago.

For example, here in Los Angeles, there are now strict new rules on the books regarding short-term rentals—rules that make it way harder to run a profitable operation—and that’s just one of the many considerations most people overlook.

It’s the economy, stupid

I don’t know why I chose to quote James Carville to kick this thing off, but his iconic catchphrase “It’s the economy, stupid” just feels so appropriate for starting this discussion about why buying a second property for Airbnb might not be such a good idea.

Today’s economy is uncertain at best. The specter of a recession still looms overhead, fueled by the recent regional banking crisis and the impending commercial real estate crisis. The Federal Reserve paused on hiking rates this month, but they’ll probably resume hiking in July. I expect the benchmark rate to hit 5.5% up from 5.25% by August 1st, which means mortgage rates will hold above 7% for residential borrowers and easily rise to over 8% for investment buyers.

In such an environment where the cost of borrowing is high, you want your rental cash flow to be as stable as possible. Yet income from Airbnb is anything but stable, as it’s subject to the whims of holidays, slow seasons, and other, unforeseen ups and downs.

Couple this unpredictability with expensive monthly mortgage payments, general operational costs (e.g., cleaners), and unforeseen maintenance (e.g., a new water heater), and the risk of buying a second home to Airbnb is simply too great to take on, save for the lucky few who can afford to conduct an all-cash purchase.

The law is coming

In the first few years of Airbnb, short-term renting was the wild west. Technology and innovation beat local governments to the punch, allowing property owners to lease their Los Angeles properties to anyone willing to pay, without the need to adhere to the rules, regulations, and taxes that impacted traditional landlords or hotels.

That was then—this is now.

Today’s Airbnb hosts face a much different reality than those of yesteryear due in large part to a number of local and state legislative measures put into place.

For example, in Los Angeles, the Home-Sharing Ordinance prohibits any listing of a short-term rental without a valid home-sharing registration number. Moreover, the same ordinance states that you aren’t even supposed to engage in short-term leasing unless the property is your primary residence and you aren’t leasing it for more than 120 days per year. Keep in mind, those are just some of the BIG rules related to short-term leasing. There are plenty of other “small rules” that add to the stress of running an Airbnb such as:

- The provision of basic health and safety features (fire extinguishers, smoke detectors, and carbon monoxide detectors, etc.),

- Prohibition of late-night outdoor parties.

- Adherence to occupancy limits.

- Publishing of on-property codes of conduct.

Then there are taxes to consider, such as Transient Occupancy taxes, Tourism Business Improvement taxes, and an emerging affordable housing tax. While many of these and other taxes are paid by guests, not all are, so it’s important to think about what your tax burden might be if you engage in short-term leasing.

These little rules and regulations add to more than the economic cost of running an Airbnb—they add to the emotional cost as well. It takes time and energy to ensure you’re running a short-term rental that’s on the right side of the law and not at risk of fines or operational suspensions.

Guests are starting to turn their back

You don’t need to look very hard to find any number of articles discussing what’s been a palpable decline in the popularity of Airbnb.

And increases in taxation and government regulation—coupled with runaway cleaning and service fees—are making Airbnb rentals often as expensive as comparable hotel rooms, if not more expensive.

Additionally, Airbnbs generally lack the amenities a hotel will provide such as a workout room, spa, and turndown service. In fact, the only thing most Airbnb hosts can hang their hat on as of right now is the provision of a “unique experience”—but in lieu of that offering, hotels appear to be offering occupants more for less money.

According to research captured in this MarketWatch article, Airbnb guests aren’t only paying more, they’re paying a lot more, with US average daily rates at $265 as of September 2022, up more than 31% since September 2019.

Supply and demand flipped

Part of what made Airbnb such a lucrative investment as recently as a few years ago was a simple imbalance between supply and demand—there were more people seeking short-term rentals on the platform than there were available hosts. This problem was especially acute in popular tourist locations such as San Francisco and Los Angeles.

The imbalance made it easier for Hosts to charge higher nightly rates and book more nights per month than what would be possible in a more balanced environment.

Unfortunately for those thinking of getting into the Airbnb leasing game today, the imbalance no longer exists.

While I won’t pretend to be a financial advisor, I’m pretty sure you’ll always have a difficult time extracting quality cash flow from an asset that’s in oversupply which Airbnb listings clearly are.

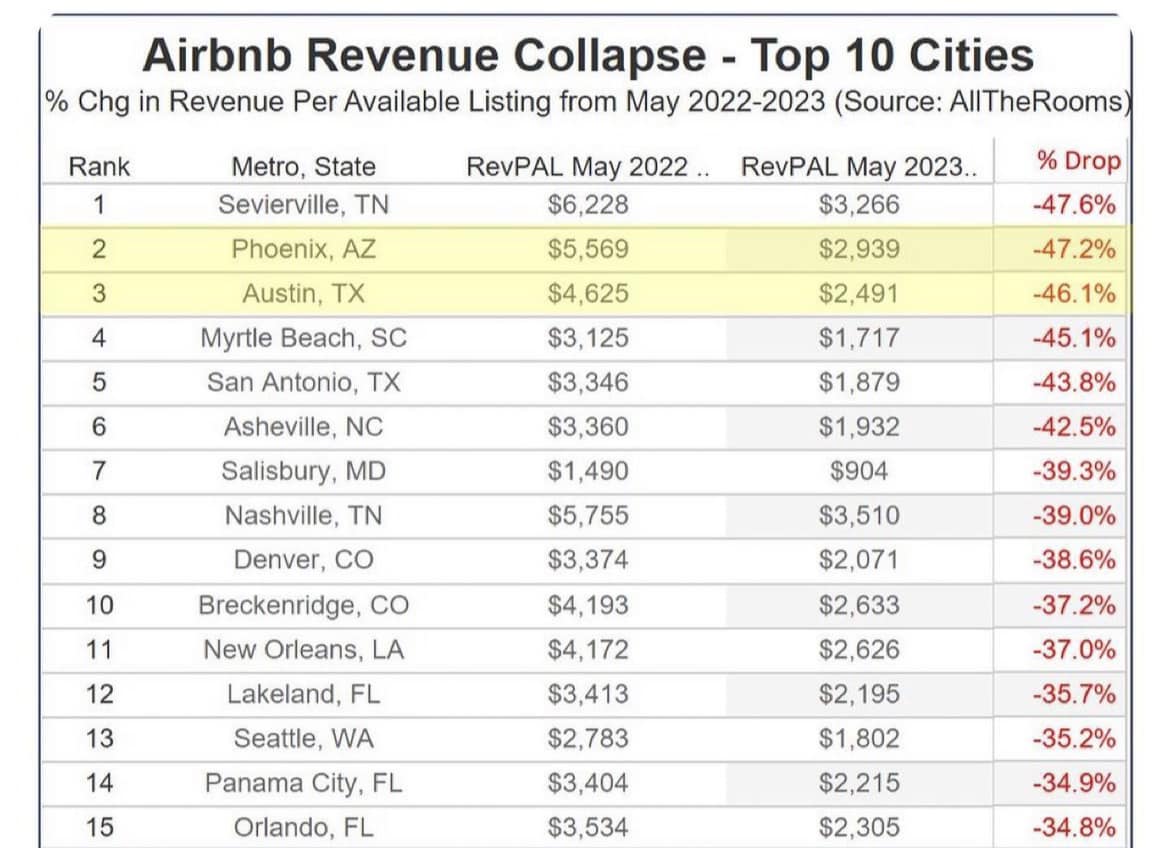

And here are some other cities in the US where AIRBNB or STR has declined significantly over the last year.

*Notice there are no cities in California, which I believe is because we have been declining throughout the pandemic and the regulation by local cities has curtailed profits.

In sum…

Buying a second home as an income property is a fine idea if you’re willing to go the traditional rental route.

Buying a second home as an income property is a terrible idea if you think you’ll make a quick buck doing short-term rentals on Airbnb.

If you’re still not convinced that buying a second property for short-term leasing is a bad idea, shoot me an email at shannonshue@kw.com or give me a call at 310-853-0335. Tell me a little bit about your situation and what you’re really looking for in an investment. From there, I can make a recommendation that best suits your needs.

-Shannon